A comparative study of the CAPM and extended models in the Indian stock market

DOI:

https://doi.org/10.14295/bjs.v3i6.545Keywords:

coskewness, cokurtosis, downside risk, upside risk, CAPM, BSEAbstract

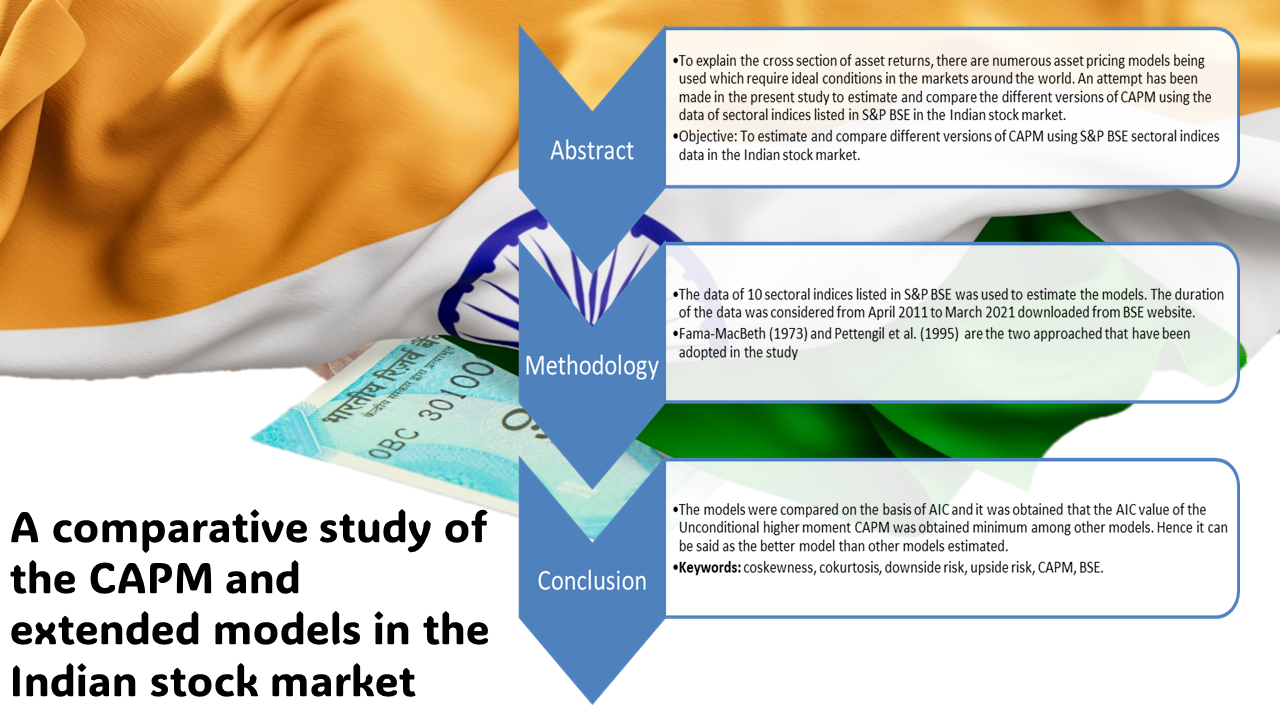

To explain the cross section of asset returns, there are numerous asset pricing models being used which require ideal conditions in the markets around the world. An attempt has been made in the present study to estimate and compare the different versions of capital asset princing model (CAPM) using the data of sectoral indices listed in S&P BSE in the Indian stock market. The two widely used approaches i.e. Fama-MacBeth (1973) and Pettengil et al. (1995) for conditional versions have been adopted in the study. The models were compared on the basis of Akaike Information Criterion (AIC) and it was obtained that the AIC value of the Unconditional higher moment CAPM was obtained minimum among other models. Hence it can be said as the better model than other models estimated.

References

Ajrapetova, T. (2018). Cross-section of asset returns: Emerging markets and market integration. European Financial and Accounting Journal, 13(1), 41-60. https://doi.org/10.18267/j.efaj.205 DOI: https://doi.org/10.18267/j.efaj.205

Akbar, M. (2013). A comparative empirical investigation of the validity of the traditional CAPM, the Higher-Moment CAPM and the Downside Risk Based CAPM in the emerging equity market of Pakistan. (Doctoral dissertation, Bahria University, Islamabad).

Ali, H. (2019). Does downside risk matter more in asset pricing? Evidence from China. Emerging Markets Review, 39(C), 154-174. https://doi.org/10.1016/j. ememar.2019.05.001 DOI: https://doi.org/10.1016/j.ememar.2019.05.001

Ang, A., Chen, J., & Xing, Y. (2006). Downside risk. The Review of Financial Studies, 19(4), 1191-1239. https://doi.org/10.1093/rfs/hhj035 DOI: https://doi.org/10.1093/rfs/hhj035

Atilgan, Y., & Demirtas, K. O. (2013). Downside risk in emerging markets. Emerging Markets Finance and Trade, 49(3), 65-83. https://doi.org/10.2753/REE1540- 496X490306 DOI: https://doi.org/10.2753/REE1540-496X490306

Atilgan, Y., Bali, T. G., Demirtas, K. O., & Gunaydin, A. D. (2019). Global downside risk and equity returns. Journal of International Money and Finance, 98. https://doi.org/10.1016/j.jimonfin.2019.102065 DOI: https://doi.org/10.1016/j.jimonfin.2019.102065

Ayub, U., Kausar, S., Noreen, U., Zakaria, M., & Jadoon, I. A. (2020). Downside risk-based six-factor capital asset pricing model (CAPM): A new paradigm in asset pricing. Sustainability, 12(17), 6756. https://doi.org/10.3390/SU12176756 DOI: https://doi.org/10.3390/su12176756

Bekaert, G., & Harvey, C. R. (2003). Research in emerging markets finance: Looking to the future. In: Emerging Markets Review, 3, 429-448 p. DOI: https://doi.org/10.1016/S1566-0141(02)00045-6

Bekaert, G., & Harvey, C. R. (2003). Emerging markets finance. Journal of Empirical Finance, 10(1-2), 3-55. https://doi.org/10.1016/S0927-5398(02)00054-3 DOI: https://doi.org/10.1016/S0927-5398(02)00054-3

Black, F. (1972). Capital market equilibrium with restricted borrowing. Journal of Business, 45(3), 444-454. DOI: https://doi.org/10.1086/295472

Chen, D., Chen, C., & Chen, J. (2009). Downside risk measures and equity returns in the NYSE. Applied Economics, 41(8), 1055-1070. https://doi.org/10.1080/00036840601019075 DOI: https://doi.org/10.1080/00036840601019075

Chhapra, I. U., & Kashif, M. (2019). Higher co-moments and downside beta in asset pricing. Asian Academy of Management Journal of Accounting & Finance, 15(1), 129-155. https://doi.org/10.21315/aamjaf2019.15.1.6 DOI: https://doi.org/10.21315/aamjaf2019.15.1.6

Fama, E., & French, K. (1992). The cross section of expected return. Journal of Finance, 47(2), 427-465. https://doi.org/10.1111/j.1540-6261.1992.tb04398.x DOI: https://doi.org/10.1111/j.1540-6261.1992.tb04398.x

Galagedera, D. U. A. (2009a). An analytical framework for explaining relative performance of CAPM beta and downside beta. International Journal of Theoretical and Applied Finance, 12(03), 341-358. https://doi.org/10.1142/S0219024909005257 DOI: https://doi.org/10.1142/S0219024909005257

Galagedera, D. U. A. (2009b). Economic significance of downside risk in developed and emerging markets. Applied Economics Letters, 16(16), 1627-1632. https://doi.org/10.1080/13504850701604060 DOI: https://doi.org/10.1080/13504850701604060

Harvey, C., & Siddique, A. (1999). Autoregressive Conditional Skewness. Journal of Financial and Quantitative Analysis, 34(4), 456-487. https://doi.org/10.2307/2676230 DOI: https://doi.org/10.2307/2676230

Hoque, M. E., & Low, S.-W. (2020). Industry risk factors and stock returns of malaysian oil and gas industry: A new look with mean semi-variance asset pricing framework. Mathematics, 8(10), 1732. https://doi.org/10.3390/math8101732 DOI: https://doi.org/10.3390/math8101732

Klebaner, F., Landsman, Z., Makov, U., & Yao, J. (2017). Optimal portfolios with downside risk. Quantitative Finance, 17(3), 315-325. https://doi.org/10.1080/ 14697688.2016.1197411 DOI: https://doi.org/10.1080/14697688.2016.1197411

Kraus, A., & Litzenberger, R. (1976). Skewness preference and the valuation of risky assets. Journal of Finance, 31(4), 1085-1094. https://doi.org/10.2307/2326275 DOI: https://doi.org/10.2307/2326275

Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7, 77-91. DOI: https://doi.org/10.1111/j.1540-6261.1952.tb01525.x

Misra, D., Vishnani, S., & Mehrotra, A. (2019). Four-moment CAPM model: Evidence from the indian stock market. Journal of Emerging Market Finance, 18(1suppl), S137-S166. https://doi.org/10.1177/0972652719831564 DOI: https://doi.org/10.1177/0972652719831564

Momcilovic, M., Zivkov, D., & Vlaovic-Begovic, S. (2017). The downside risk approach to cost of equity determination for Slovenian, Croatian and Serbian capital markets. Ekonomie a Management, 3, 147-158. https://doi.org/10.15240/tul/001/2017-3-010 DOI: https://doi.org/10.15240/tul/001/2017-3-010

Narayan, P. K., and Ahmed, H. A. (2014). Importance of skewness in decision making: evidence from the Indian stock exchange. Global Finance Journal, 25(3), 260-269. https://doi.org/10.1016/j.gfj.2014.10.006 DOI: https://doi.org/10.1016/j.gfj.2014.10.006

Pla-Santamaria, D., & Bravo, M. (2013). Portfolio optimization based on downside risk: A mean-semivariance efficient frontier from Dow Jones blue chips. Annals of Operations Research, 205(1), 189-201. https://doi.org/10.1007/s10479-012-1243-x DOI: https://doi.org/10.1007/s10479-012-1243-x

Rubinstein, M. (1973). The fundamental theorem of parameter preference security valuation. Journal of Financial and Quantitative Analysis, 8(1), 61-69. https://doi.org/10.2307/2329748 DOI: https://doi.org/10.2307/2329748

Rutkowska-Ziarko, A., Markowski, L., & Pyke, C. (2019). Accounting beta in the extended version of CAPM. In: Contemporary trends and challenges in finance, Springer, 147-156 p. https://doi.org/10.1007/978-3-030-15581-0_14 DOI: https://doi.org/10.1007/978-3-030-15581-0_14

Salah, H. B., Chaouch, M., Gannoun, A., De Peretti, C., & Trabelsi, A. (2018). Mean and median-based nonparametric estimation of returns in mean-downside risk portfolio frontier. Annals of Operations Research, 262(2), 653-681. https://doi.org/10.1007/s10479-016-2235-z DOI: https://doi.org/10.1007/s10479-016-2235-z

Sauer, A., & Murphy, A. (1992). An empirical comparison of alternative models of capital asset pricing in Germany. Journal of Banking and Finance, 16(1), 183-196. DOI: https://doi.org/10.1016/0378-4266(92)90084-D

Tsai, H., Chen, M., & Yang, C. (2014). A time-varying perspective on the CAPM and downside betas. International Review of Economics and Finance, 29(C), 440-454. https://doi.org/10.1016/j.iref.2013.07.006. DOI: https://doi.org/10.1016/j.iref.2013.07.006

Vishnani, S. (2013). Asset pricing and co-skewness risk: evidence from India. Afro-Asian Journal of Finance and Accounting, 3(3), 208-221. DOI: https://doi.org/10.1504/AAJFA.2013.054423

Wolfle, M., & Fuss, R. (2010). A higher-moment CAPM of Korean stock returns. International Journal of Trade and Global Markets, 3(1), 24-51. https://doi.org/10.1504/IJTGM.2010.030407 DOI: https://doi.org/10.1504/IJTGM.2010.030407

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2024 Akash Asthana, Syed Shafi Ahmed

This work is licensed under a Creative Commons Attribution 4.0 International License.

Authors who publish with this journal agree to the following terms:

1) Authors retain copyright and grant the journal right of first publication with the work simultaneously licensed under a Creative Commons Attribution License that allows others to share the work with an acknowledgement of the work's authorship and initial publication in this journal.

2) Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the journal's published version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgement of its initial publication in this journal.

3) Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work.